The Credit Application: Your First Line of Defense

Last month we covered building your credit policy framework. A cannabis credit application is how that policy meets the real world.

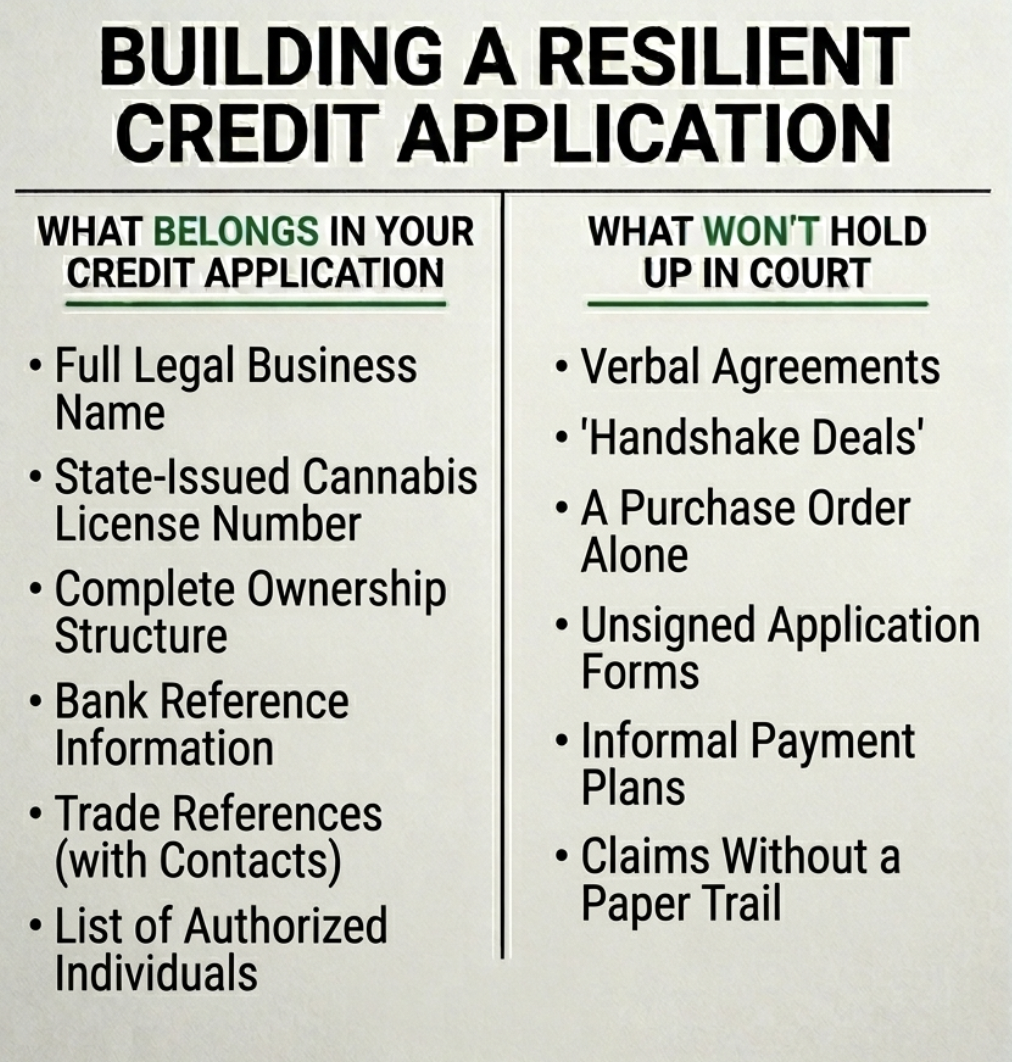

A verbal agreement is not a credit policy. A purchase order is not a guarantee of payment. In cannabis B2B, where banking access is limited, operator turnover is high, and invoice amounts can be substantial, a handshake deal creates exposure that you will feel the moment an account goes sideways. The credit application is the document that closes that gap before the first unit ships on terms.

What Is a Cannabis Credit Application?

A cannabis credit application is a formal document that collects the financial, legal, and operational information required to evaluate a customer before extending trade credit.

More importantly, it creates a paper trail that protects your business if a debt goes unpaid.

What Should a Cannabis Credit Application Include?

A properly structured credit application collects everything you need to make an informed credit decision and, just as importantly, everything you need to act if a debt goes unpaid.

That means:

Full legal business name

Principals and ownership structure

State-issued cannabis license number

Bank reference information

Trade references with contact details

Names of individuals authorized to charge on behalf of the account

Every field matters.

Why a Cannabis Credit Application Matters for Collections

The paper trail a signed credit application creates is not just administrative. It is the foundation of your collections and legal escalation strategy.

When a debt ages past 90 days and you need to pursue recovery, a documented credit application tells a collections agency who the principals are, where they bank, and who else in the industry has extended them credit. Without it, you are chasing a business name with no face behind it.

For a closer look at what that exposure looks like, CannaBIZ Collects' overview of dispensary liability is a useful reference on how quickly informal arrangements become legal questions.

Late Fees and Collection Cost Clauses in Cannabis Credit Applications

Your credit application is also where you establish the right to recover late fees and collection costs—one of the most overlooked protections in cannabis B2B.

To be enforceable, these terms must be agreed to in writing before the debt is incurred.

That means the credit application needs to explicitly state:

The late fee structure (e.g., 1.5% per month after 30 days)

When those fees begin

That the debtor is responsible for collection and legal costs

The language needs to be clear and specific. Courts will not enforce vague or punitive terms. The goal is to position these fees as reimbursement for the cost of managing delinquent accounts.

Consistency and Legal Review

Consistent enforcement matters.

If you routinely waive late fees for certain accounts, you weaken your ability to enforce them against others. State laws also cap interest rates and fees in most jurisdictions, so your credit application terms should always be reviewed by legal counsel.

A well-drafted clause protects you. A poorly drafted one gets dismissed when you need it most.

Personal Guaranties in Cannabis Credit

Your credit application is also the right place to embed personal guaranty language, requiring a principal to personally back the business obligation.

We will go deeper on personal guaranties in a future issue, but the key takeaway is simple:

This protection only exists if:

The language is included in the application

The agreement is signed before the first order

Using Credit Data to Strengthen Decisions

Once you have collected the data, the Cannabiz Credit Association can help you put it to work.

CCA scores applicants using payment performance data sourced from member creditors across the cannabis industry, giving you a benchmark that trade references alone cannot provide.

Your credit policy sets the criteria. The data tells you if the applicant meets it.

Final Check Before Extending Credit

Do you have a signed cannabis credit application on file for every active account?

Does it include enforceable late fee and collection cost language?

If the answer to either question is no, that is where to start.

CannaBIZ Collects partners with the Cannabiz Credit Association to help clients turn credit applications into credit intelligence.

Visit cannabizcollects.com.

Disclaimer

This section is for educational purposes only and does not constitute legal advice. Consult a licensed attorney to ensure your credit application terms comply with applicable state and federal law.